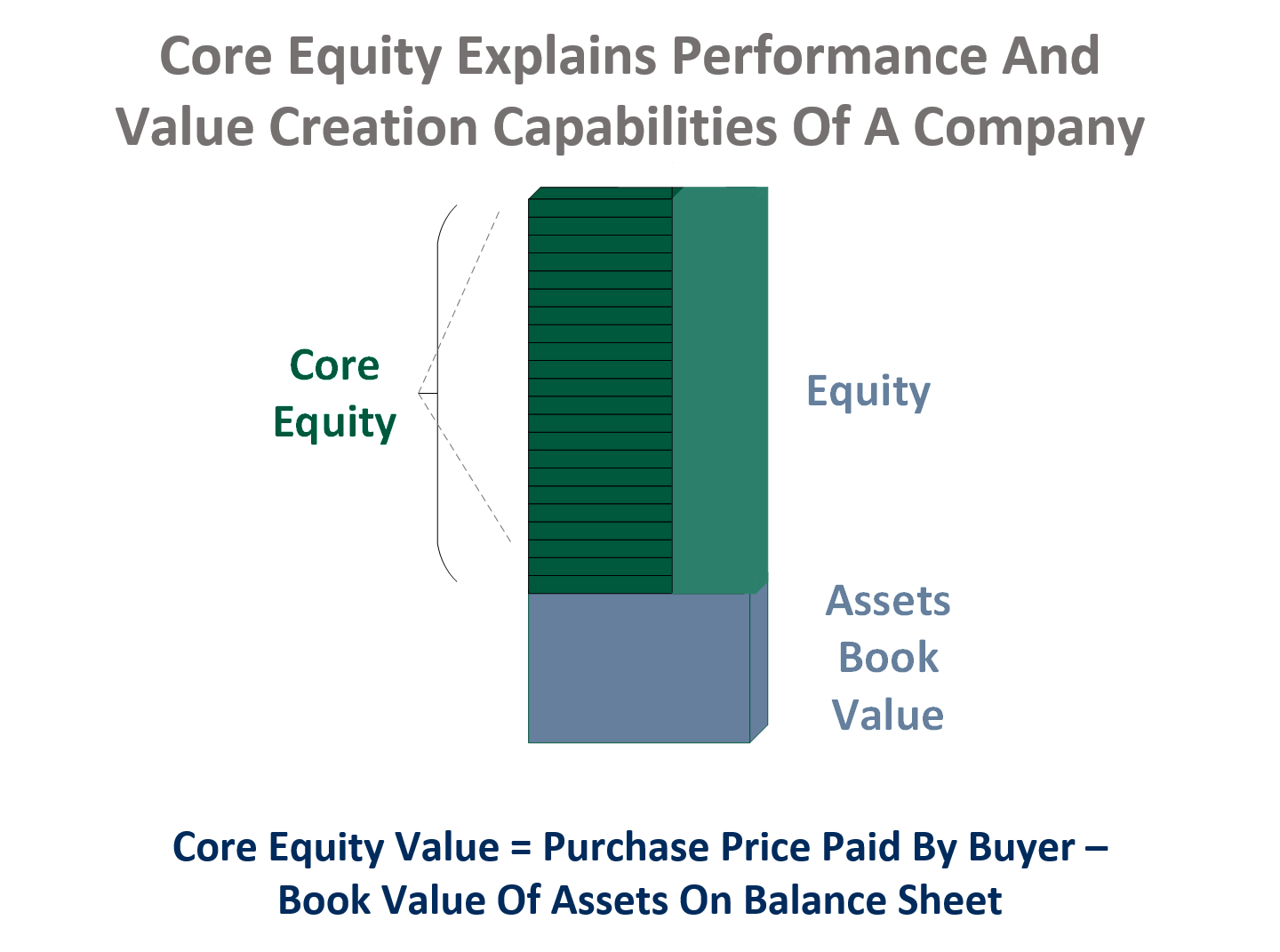

Core Equity Value

Core Equity Value is the amount a buyer pays for a company over the book value of assets on the balance sheet. Another way to view core equity value is it is the premium a buyer is willing to pay for the company. (In accounting terms, this is referred to as “goodwill.”) The concept is you create core equity value deliberately so that it is not merely a byproduct of doing business as usual. If you put core equity under a microscope, you would see the specific functions and capabilities that create value and explain a company’s performance. Business owners who intentionally create core equity value build more valuable companies.

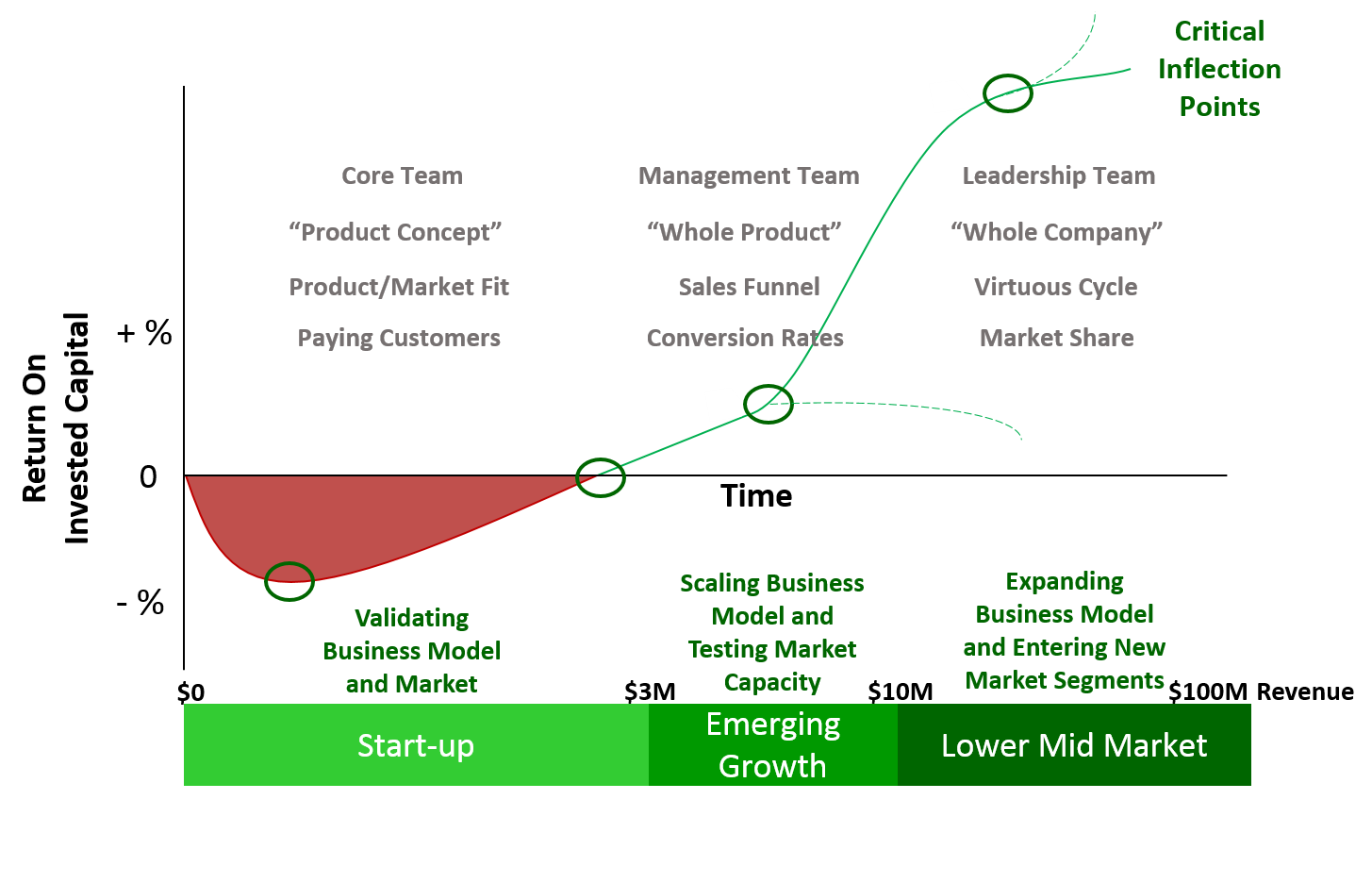

Evolution of Core Equity Value

There are four critical inflection points on the path to building core equity value:

- Making the first dollar of revenue

- Breaking-even (cash flow positive)

- Taking-off

- Leveling-out … and retuning

These inflection points correspond to three major phases of growth.

Start-up Phase

During the Start-up phase, the entrepreneur forms a “Core Team” to craft the initial business model and begins to zero-in on a market segment by developing a “product concept” for which customers are willing to pay. In general terms, the Start-up phase is characterized by revenue between $0 and $3 million. Reaching $3 million is significant because it yields sufficient funds to begin building out the business model so that it can scale. It is important to note, however, that many companies – particularly lifestyle companies – may choose to remain just the size they are and not make the investment required to move to the next growth phase. This choice is fine as long as doing so satisfies the entrepreneur’s corporate and personal objectives.

Emerging Growth Phase

The Emerging Growth phase spans from $3 million to $10 million in revenue. This phase tests the business model’s capacity to scale and the market’s capacity to deliver more customers. If both of these pursuits are successful, revenue takes off. Otherwise, growth hits a plateau and will eventually decline unless adjustments to the business model or the market segment are successfully made. The product concept is turned into a more complete and “whole product” and a “Management Team” takes shape to cover key functional areas. This revenue range tests both the soundness of the business model as well as the breadth of the market.

Lower Middle Market

The Lower Middle Market spans $10 million to $100 million in revenue. Relatively few companies make it across the $10 million threshold allowing entry into the Lower Middle Market, where greater exit values reside. Companies entering the Lower Middle Market now have the resources to build-out a more complete business and tap additional market segments. In this stage, the business model is made more versatile and resilient by forming a “whole company” and building out the organization chart. Organic growth is driven through product expansion, the ability to care for existing customers, and the wherewithal to capture new customers. Acquisitions can also play a critical role to expedite growth. The management team undergoes a transformation into a “Leadership Team” as leadership functions are extended beyond just one or two key individuals. The $10 million mark is important because companies of this size get on the radar screens of financial and strategic buyers. The $100 million mark is significant because this is the point where many people believe a company may be of sufficient size to make an Initial Public Offering potentially viable. (It is important to note, however, that IPOs make up only 1% of growth and exit transactions and a lot of complex factors determine if and when a company should be taken public.) Companies in the Lower Middle Market have more options, choices, and complexities when it comes time to plan an exit.

Growth Curve

Producing a growth curve versus one that is flat requires an integrated business model that can scale and a market that can support the growth potential of the company. Four key business drivers support growth curves: strategic positioning, market development, sales execution, and operational excellence. Companies who are able to translate these business drivers into executable road maps build core equity value. In turn, this increases the likelihood of producing an upward slopping growth curve.

Company Value

Knowing what the company is worth is a fundamental piece of knowledge and key to measuring a company’s performance over time. Unfortunately, there are multiple ways of calculating a company’s worth, some of which are rudimentary (and misleading) and others that are more complicated. We can look to Warren Buffett, who knows a thing or two about valuing a business, for guidance: the value of a business resides in the company’s ability to generate future cash flows that can be taken out of the business after adjusting for time and risk. This figure that Warren Buffett relies upon is a company’s intrinsic value and, as noted in Valuing Private Companies, it is the proper way to value a company. The challenge lies in constructing a model that reasonably estimates these future cash flows. The model typically takes the form of a 5 year pro forma that forecasts a company’s income statement and balance sheet. But this is more than a mathematical exercise. Properly building a 5 year pro forma requires analyzing the competitive environment, understanding the strengths and opportunities the company possesses, dissecting the weaknesses and threats the company faces, and evaluating the dynamics of the industry and markets in which the company competes. Knowing your company’s intrinsic value gives you a baseline to measure your progress and to better understand what creates (and destroys) value.

Return On Invested Capital

Knowing what a company is worth tells only half the story. You also need to factor in the amount of capital (both debt and equity) that has been invested into the company to get a clear understanding of the company’s true value. By knowing the “free cash flows” of the company and the amount of capital invested into the company, we can calculate the Return On Invested Capital. These two metrics – intrinsic value and Return On Invested Capital – are the preferred methods sophisticated buyers use to assess the overall value and performance of a company.