Valuing Private Companies That Are Medium-size Businesses

Understanding how sophisticated buyers value a private company is critical to building a more valuable business. Valuing a medium-size company is a complex process. The standard method used by investment bankers is to apply three different approaches to determine the company’s enterprise value, which is usually expressed as a range of multiples of EBITDA. EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization and is a standard way of measuring a company’s cash flow. For instance, a company with $4 million in EBITDA and a range of multiples of 4.5X – 5.5X has a valuation range (i.e., enterprise value) of $18,000,000 to $22,000,000. Each approach’s range of value is then superimposed on the others and the overlapping areas indicate the likely value of the company.

- Comparable Companies approach (also known as “trading comps”) compares the company to a subset of public companies in the same industry with similar products and services. The premise is that these companies share similar business and financial characteristics. Public companies are used because there is abundant and detailed financial and market data available to compare the companies. Ideally, private companies similar in size and in the same industry would also be used for benchmarking comparisons. However, by virtue of being private, they do not share detailed financial and market information. The challenge and drawback of using comparable companies analysis is trying to compare a multi-billion dollar company to a relatively much smaller private company. (Comparable companies analysis is much more effective comparing a public company to other public companies.)

- Precedent Transactions approach (also known as “transaction comps”) compares the company to what was actually paid to purchase similar companies. The premise is quite sound: this is what the market determined the prices were for companies bought over the last two to three years that were of a similar size and in a similar business. The challenge with this approach is the purchase price and other relevant information are not disclosed for the vast majority of private company acquisitions. Specifically, 74% of strategic acquisitions are made by private companies that are under no obligation to disclose purchase price details. As for public companies, a large portion of acquisitions end up being classified as “immaterial,” which means they do not have to disclose detailed information on the transaction. Consequently, while the number of transactions is known, the details behind the transactions (i.e., purchase price, deal structure) are hidden for the majority of deals.

- Discounted Cash Flow (DCF) approach evaluates the value of future cash flows. The premise is that the value of the company is the result of future earnings, specifically free cash flow. A five year forecast of future earnings is made taking into account sales growth, profit margins, capital expenditures, and working capital and including all tangible and intangible aspects of the business. These future cash flows are then discounted to adjust for time and risk. The resulting present value is the company’s intrinsic value, which is another way of saying what the company is worth. The challenge with the DCF method is modeling future cash flows requires in-depth analysis, which is complex and time consuming.

For the majority of private companies, of the three approaches described above, the Discounted Cash Flow analysis is clearly the preferred method. All too often, Comparable Companies analysis suffers from comparing apples to oranges, while Precedent Transactions analysis struggles with a paucity of data since only a small number of deals disclose the purchase prices paid for the companies.

Financial and strategic buyers are picky and highly selective. Since only 0.2% (0.002) of private companies in the U.S. successfully execute Private Capital Market transactions each year, it is definitely a “buyers” market. A U.S. Chamber of Commerce study provides additional evidence to the selectivity of the Private Capital Markets by noting that Merger & Acquisition (M&A) advisors disqualified 65% to 75% of prospective sellers.

Valuing Smaller-size Companies

In the world of small business, there are three common approaches to business valuation.

- The income approach determines value based on the company’s ability to generate future earnings that business owners can take out of the company (this is how owners get “paid”).

- The asset approach determines the value of the company based on the fair market value of assets less the company’s liabilities.

- The market-based approach compares the company to historic sales involving similar businesses and relies on “pricing multiples” to determine a potential selling price.

These three approaches have similarities to the approaches described above for medium-size companies, but there are notable differences. A key metric in small business transactions is Seller Discretionary Earnings. SDE is a broadly accepted approach to “recasting” a small business’s earnings to adjust for owner-operator expenses. To complicate matters, SDE is different from EBITDA, which is different from Adjusted EBITDA, which is different from “earnings” reported on tax returns. The key takeaway is that there is a well established approach for valuing and selling small businesses that has been refined over several decades. The other key takeaway is that the approach to valuing and selling medium-size businesses is notably and substantially different and more complex.

Drawing The Line Between Small and Medium-Size Businesses

Size does matter when it comes to valuation. There is not a universal set of criteria that precisely defines a “small” business. For example, the U.S. Government defines a small business as companies with 500 employees. In many respects, a company with 500 employees is a large company.

A more meaningful line of demarcation than the number of employees is the amount of annual revenue marking entry into the Lower Middle Market. Once again, there is not a universal standard precisely defining the Lower Middle Market, but two of the most prevalent ranges are $5M to $50 million and $10M to $100 million. Using the latter range, only 5% of U.S. companies cross this threshold. Consequently, $10 million marks a good dividing line for designating a “medium-size” company and the entry point to the Lower Middle Market.

Investment bankers, who specialize working with medium-size companies in the “Lower Middle Market,” and business brokers, who specialize working with smaller-size companies making up the “Main Street” market segment, prefer using the value of a company to determine if the company falls on the Main Street side of the ledger or resides in the Lower Middle Market. Knowing the correct market segment a company belongs in is important because it is central to selecting the proper transaction intermediary. Business brokers take a different approach to selling a company than investment bankers, whose process is more involved, time consuming, complex, and expensive. There is not an iron clad rule separating Main Street from the Lower Middle Market. Companies with a valuation below $2 million are clearly in Main Street territory, while companies with a valuation above $10 million are clearly in the Lower Middle Market. In between $2 million and $10 million, however, some companies may be better suited using a business broker while other companies may be better served using an investment banker as the transaction intermediary. The growth profile of a company is the key determinant; a company with a strong growth profile in an attractive industry is a more likely candidate for an investment banker. A transaction intermediary, however, is not a requirement. In many circumstances a transaction intermediary is not needed, while in other situations they can add terrific value.

An added layer of complexity exists because there are several terms used to denote a company’s “value.”

- The “market value” of a company is the price that a willing buyer and a willing seller agree upon. For public companies, this price is only a ticker symbol away and is instantly accessible. However, this is not the case for privately-held companies for which the market price is only determined through a lengthy process of discovery, due diligence, and negotiation. Consequently, the “market value” price is not readily or easily available and is only known for certain after the deal has closed.

- The “enterprise value” of a company is the total value of a company taking into consideration both equity and debt. This term is most commonly associated with valuing public companies and represents the theoretical takeover price an acquirer would have to pay. Because a publicly traded company’s financial data is readily available, the information exists to calculate and publish the enterprise value daily. For privately-held companies, the concept of enterprise value is equally relevant: it is the theoretical price a buyer would have to pay to acquire the company. Unlike a public company, the enterprise value for a private company is not readily available nor is it constantly updated.

- The “intrinsic value” of a private-held company (discussed in the first section above under Discounted Cash Flow) is essentially the same as the enterprise value. For valuation purposes, a company’s intrinsic value can be calculated and is typically expressed as a range.

So, which of these values are best used for determining if a company qualifies to be in the Lower Middle Market? The “intrinsic value” is the proper value to use. However, the process of determining a company’s intrinsic value is complex and time consuming. Consequently, people look for quicker and easier ways to estimate a company’s value, but the results can be misleading.

Understanding Multiples

There is a lot of confusion over using “multiples” to estimate a company’s value. A company’s intrinsic value is based on the fundamentals specific to a given company and its ability to generate future cash flows and this is the proper way to value a company. Consequently, multiples do not establish a company’s intrinsic value. It is the other way around. A company’s intrinsic value establishes the multiple. Focusing on a multiple – either based on an industry average or using what was paid for another company – instead of focusing on the specific company’s “intrinsic value” can lead to concluding that a company is worth more than can be substantiated based on the company’s inherent fundamentals and future outlook. It works the other way around, too. Relying on multiples can understate the intrinsic value of a company resulting in a business owner being paid less than he or she should be.

Complicating matters is that multiple multiples exist. The three most common multiples are (1) EBITDA, (2) revenue, and (3) SDE. The Seller Discretionary Earnings multiple is only used by business brokers and applies to smaller “Main Street” companies. EBITDA is the most prevalent multiple used in the Lower Middle Market.

Multiples are used as shorthand providing a quick and convenient way to quote a company’s value without citing the actual dollar amount. For example, a “5X” multiple of EBITDA is the same as saying the company is valued at $20 million, provided you know the EBITDA for the company is $4 million. Since buyers often price a company based on multiples of EBITDA (typically using the last twelve months) it is natural to associate the value of the company with the multiple. At the end of the day, however, it is the absolute dollar amount that counts (and gets wired); multiples provide an easy to use method to calculate that dollar amount.

Multiples make it easy to compare one company to another in the same industry. So if a business owner knows the average range of multiples in the company’s industry is 5X – 7X, he or she can estimate what the company is worth. But this approach to determining a specific company’s valuation can be very misleading. It is important to keep in mind that averages are composed of many companies, some of which are valued 25% higher than the average and others 25% lower than the average. Where a particular company falls relative to an “average” is due in large part to the fundamentals of the company and its ability to generate future cash flows. (There are many other factors that have a significant bearing on a company’s ultimate market value … see Exit Timing and Core Equity Value.)

The Difference Between Intrinsic Value and Market Value

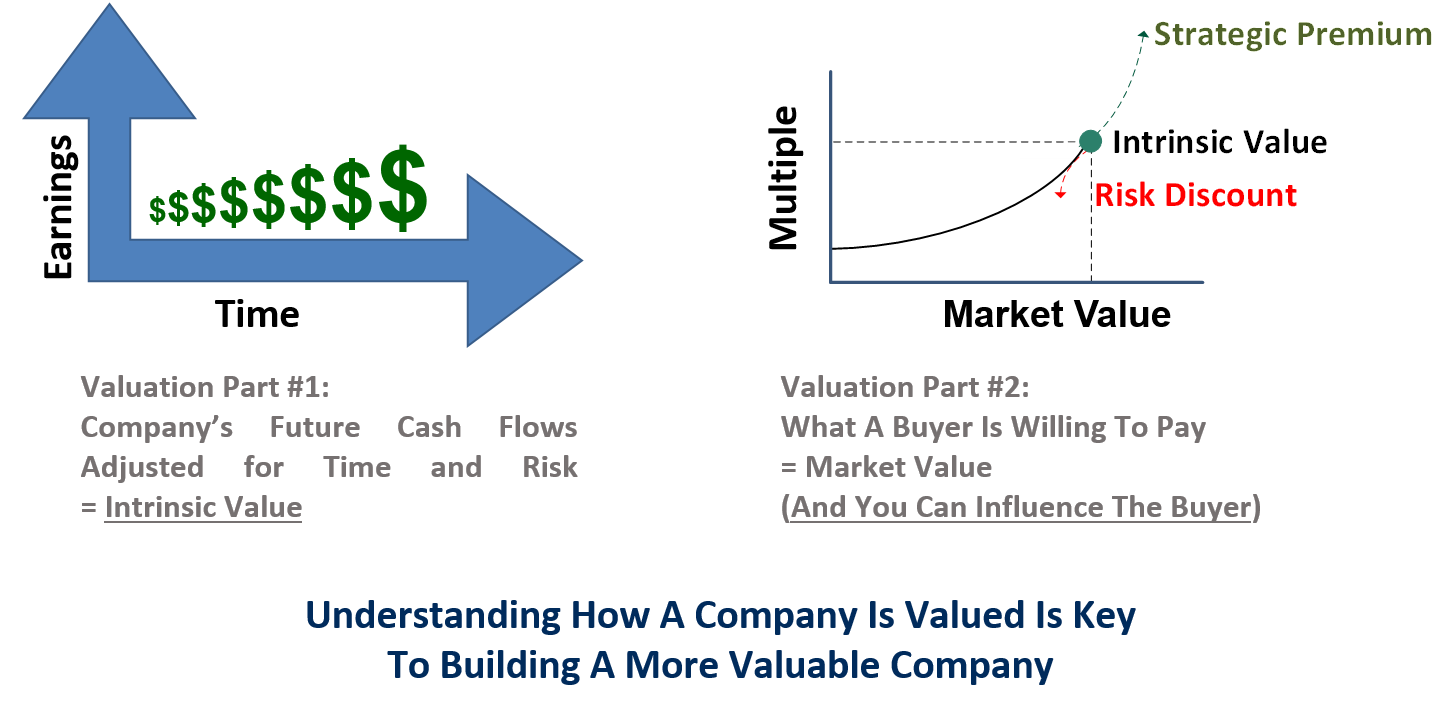

There are two parts to determining the market value of a medium-size privately-held company. Part #1 is forecasting a company’s future cash flows and then applying some math to adjust for “time and risk” (also known as determining the present value). The challenge is that there are many factors that impact a company’s ability to produce future cash flows starting with the industry the company is in, the company’s inherent capabilities and its position in the industry, its ability to carve out a competitive advantage, interplay between suppliers, customers, and competitors, and the overall economic environment (i.e., recessions). A company needs to look beyond past trends and focus on what specifically the company will do to produce cash flows in the future. The ability to document, explain, and defend how cash flows will be generated in future years in a credible and authentic manner is the very core of establishing a company’s intrinsic value. But not all future cash flows are the same. Cash flows that are more predictable and growing are more valuable than cash flows that are not predictable and fluctuate a lot. This is one of the key reasons that using multiples as the basis for valuing a company is inferior to using a company’s intrinsic value — what matters are the future cash flows of a specific company and not what the “average” multiple for an industry might be. Business owners who can document how they are actually going to generate future cash flows are in a much stronger position than a business owner who simply relies on “industry average multiples” and past trends. Furthermore, a business owner who can explain and defend the intrinsic value of the company is able to quickly assess if a proposed purchase price is reasonable or not. This is where the second part figures into the equation.

Part #2 is knowing there is not just “one” price that determines what a private company is worth. Instead, multiple prices exist for the same company with each price, in part, depending on the “eyes of the beholder” of each prospective buyer. Some buyers may see how combining the company with the prospective buyer’s other products, services, assets, customers, suppliers, and capabilities can produce “synergies” leading them to place a higher valuation on the company compared to other prospective buyers. On the other hand, if there are blemishes in the company, or if there is greater perceived risk and uncertainty, then a prospective buyer will apply “discounts,” which lowers the company’s valuation. A major part of building a more valuable company is knowing what specifically leads to commanding a strategic premium and how to limit risk discounts. Market value is ultimately determined by what a buyer is willing to pay … and you can influence the buyer.

Why Price And Value Are Not The Same

While it may seem counter intuitive, the “price” (market value) of a company is usually different from the “value” (intrinsic value) of a company. Finding the “best” buyer requires considering a broad variety of factors. What a buyer is willing to pay – and how the payment is structured – is obviously important. Knowing how a particular offer compares to the intrinsic value of a company is central to assessing how favorable or unfavorable an offer truly is. The price of a company can be driven higher, and sometimes substantially higher, by creating a competitive deal environment where two or more qualified buyers are bidding for the company (see ExitHigh Plan). Additionally, the timing of a transaction has a significant effect on the “price” of the company (see Exit Timing). At the end of the day, the market determines the price of a company and not the business owner. The business owner, however, influences higher prices by demonstrating how the company’s core equity value increases value that matters to each prospective buyer. Ideally, the business owner is rewarded with multiple prices exceeding the intrinsic value of the company.

Knowing Your Value

Sophisticated buyers (see Private Capital Markets) construct detailed models to estimate future cash flows and to derive the intrinsic value of a company. This intrinsic value may then be adjusted upward to reflect a strategic premium or adjusted downward to discount for areas of risk and uncertainty. The resulting intrinsic value is then used to determine a rate of return on the investment the buyer is making in purchasing (or investing in) the company. Sophisticated buyers will also cross-check the intrinsic value with relevant precedent transactions of companies of a similar size and in the same industry that were sold in the past three years for which they have detail knowledge of the purchase price and deal structure. While the resulting intrinsic value may be quoted as a multiple, at the end of the process a specific dollar price is negotiated and paid. It is ultimately this purchase price that matters (and how it is structured) and not the multiple per se.

From a valuation perspective, a company with a strong revenue growth trajectory and no current earnings may be valued considerably higher than an established company making profits, but with flat or declining growth. Because valuation is not straightforward and depends on a lot of interacting factors, valuing companies can be confusing, complex, and counter intuitive. Business owners that avoid valuation shortcuts and take the time to understand how medium-size companies are valued – and what specifically drives value that matters in their company for their particular industry – take a big step forward to building a more valuable company.

An essential management tool for building a more valuable medium-size company is a comprehensive 5 year pro forma model incorporating discounted cash flow analysis. Three benefits accrue to a business owner who properly constructs a 5 year pro forma model:

- The business owner knows what his or her company’s intrinsic value is at all times.

- Management can document, explain, and defend how future cash flows will be produced, which goes a long way towards substantiating a company’s value to sophisticated buyers.

- Management has a model to use to test different strategies to determine if they are value enhancing or value destroying.